2021 trucking forecast: ‘Partly cloudy’ with a chance of computer chips

Halfway through 2021 and more than a year since the COVID-19 pandemic began in the U.S., the trucking freight economic outlook for the rest of the year is “still partly cloudy,” according to Don Ake, VP of commercial vehicles for FTR Transporation Intelligence. “A lot of people would say it’s still mostly cloudy.”

Like a partly- or mostly-cloudy weather forecast, there is good news and bad news, depending on how it’s interpreted. The good news is OEMs have shown they are ready and able to boost vehicle production once they get essential components such as semiconductor computer chips, the scarcity of which is clogging vehicle supply chains. “As this goes on, the OEMs are becoming more adept at operating under uncertain supply conditions,” Ake said on July 1 during FTR’s monthly market update webinar.

While there are some indications that the computer chip shortage could ease later this summer, reporting on that is mixed. That is part of the bad news on the supply chain side for fleets waiting on new vehicles to meet the increasing freight demand across the U.S. “Spot rates and freight growth are continuing at high levels,” Ake said. “Things are great in the industry. We just have to build more trucks.”

Along with a sluggish supply chain, raw material costs have jumped this year and are remaining high, boosting equipment prices. “And eventually, if the prices remain high, according to the laws of supply and demand, it’s going to cut into sales at some point,” Ake warned. “Right now, things are so hot in the industry, and freight is so strong, that’s kind of just being covered over. At some point in the future, it could be an issue, but we don’t have to worry about that for now—but it’s still bad news in the industry because it’s hurting OEM and supplier profits.”

Manufacturers are also struggling with worker shortages, which could hurt demand. But Ake expects those shortages to lessen by September when the remaining COVID stimulus benefits run out. “But right now, when you add that to the mix of the supply chain, it still constricts things.”

While the supply chain is still working out kinks created during the height of the pandemic, the economy is booming.

The U.S. economy’s rebound out of the pandemic recession of 2020 is continuing after “an excellent quarter of 6.4% growth” to start the year, Ake said. That growth continued in Q2 of 2021, which FTR forecast to be 7.9% once all the data is available. According to Ake, the transportation intelligence firm expects that growth to tail off the second half of the year with 3.6% growth in Q3, followed by 3.9% growth in Q4.

According to FTR analysis, the growth of GDP goods in transportation—the portion of national GDP that generates freight—is expected to grow at an even faster rate this year. The firm forecasts a 12.2% growth in Q2, followed by 4.6% and 6% growth in the final two quarters of 2021. “Now you’re comparing year-over-year against the pandemic,” Ake cautioned. “But remember, in Q2 last year, there was still freight moving.”

That transport GDP growth is boosting truck freight, Ake said. So much so that FTR’s forecast pegs truck freight growth at 14.5% in Q2. While Ake cautioned that number isn’t final, he said, “we do know it was great. And then you see in Q3 and Q4, based on those GDP numbers, we’re looking at 7% freight growth followed by 6% growth. This is going to be an excellent freight year once again.”

Chip shortage forecasts mixed

The transportation equipment supply chain remains clogged, Ake said, citing an analogy he made months ago: “It’s like being on the highway in a massive traffic jam. At certain points, traffic is going to move better. And at certain points, traffic’s going to be stuck. That’s how it’s gone this year—where we have good months and bad months.”

Semiconductor chips continue to be the No. 1 cause of supply chain jams limiting Class 8 vehicle production, Ake said. And information is mixed about how soon this crucial link in vehicle manufacturing supply chains will flow again. In June, CNBC reported that semiconductors would begin flowing to auto manufacturers by August. But a day later, Susquehanna Financial forecast that semiconductor wait times are getting worse with a lead time of 25 weeks. Then last week, Intel CEO Pat Gelsinger said the chip shortage could last until 2023.

“So it’s hard to know what to think,” Ake said. “I tend to believe CNBC is getting good data because they’re telling people to invest in the automakers off that information. So they have reputations to defend. But the bottom line is we do not know when this will end, and until this gets going, it’s going to restrict production to some extent.”

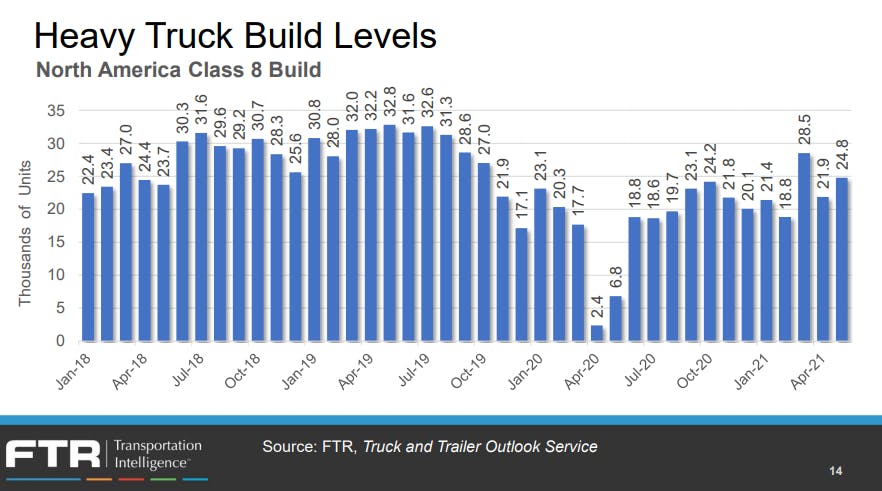

Heavy-duty vehicle builds have teetered between 18,000 and 29,000 this year because of the unreliable supply chain, which Ake said is “going to be an issue going forward.” Parts supply needs to improve soon to match FTR’s positive outlook for truck builds in the second half of 2021.

As of July 1, FTR was forecasting 307,400 new Class 8 vehicles built this year, followed by 340,000 in 2022 and 350,000 in 2023. This forecast, particularly for Q3 and Q4 2021, has more downside risk than upside, Ake said. The 2022 forecast could increase more if demand isn’t met in 2021.

“We are monitoring the build situation very closely,” Ake said. “We’re to the point where we need to see improvement very soon in order for things to move forward and for our forecasts and what the OEMs are planning to build to come to fruition.

Looking at medium-duty vehicle production, Ake said the semiconductor shortage is finally hitting that sector as April Classes 6 and 7 numbers were weak and are expected to be constricted for months. Part of this is because OEMs are not making medium-duty builds a priority for computer chip distribution.

While demand builds for MD trucks, production should ramp up once the supply chain opens and it plays catch-up later this year and into 2020, Ake noted. FTR is currently forecasting about 215,000 Class 4-7 builds in 2021, growing to 238,000 in 2022 and 250,000 in 2023.

Source: fleetowner.com, by Josh Fisher

{kind=link}

{kind=link}